Cite this document

(Describe the various stages of the typical lifecycle of an individual Essay, n.d.)

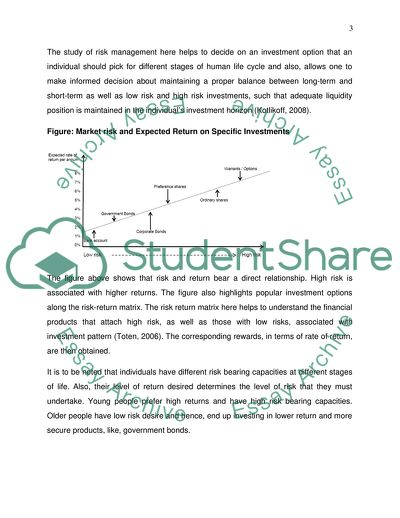

Describe the various stages of the typical lifecycle of an individual Essay. https://studentshare.org/finance-accounting/1806918-describe-the-various-stages-of-the-typical-lifecycle-of-an-individual-in-the-uk-today-and-identify-the-most-relevant-financial-products-that-should-be-considered-at-each-stage

Describe the various stages of the typical lifecycle of an individual Essay. https://studentshare.org/finance-accounting/1806918-describe-the-various-stages-of-the-typical-lifecycle-of-an-individual-in-the-uk-today-and-identify-the-most-relevant-financial-products-that-should-be-considered-at-each-stage

(Describe the Various Stages of the Typical Lifecycle of an Individual Essay)

Describe the Various Stages of the Typical Lifecycle of an Individual Essay. https://studentshare.org/finance-accounting/1806918-describe-the-various-stages-of-the-typical-lifecycle-of-an-individual-in-the-uk-today-and-identify-the-most-relevant-financial-products-that-should-be-considered-at-each-stage.

Describe the Various Stages of the Typical Lifecycle of an Individual Essay. https://studentshare.org/finance-accounting/1806918-describe-the-various-stages-of-the-typical-lifecycle-of-an-individual-in-the-uk-today-and-identify-the-most-relevant-financial-products-that-should-be-considered-at-each-stage.

“Describe the Various Stages of the Typical Lifecycle of an Individual Essay”. https://studentshare.org/finance-accounting/1806918-describe-the-various-stages-of-the-typical-lifecycle-of-an-individual-in-the-uk-today-and-identify-the-most-relevant-financial-products-that-should-be-considered-at-each-stage.